by

by UK National Insurance Contributions for Businesses: 2026 Rates, Calculations & Compliance

22 May, 2026Running a business in the United Kingdom means juggling more than just payroll and profit margins. There is a silent partner in every paycheck you issue: National Insurance Contributions are mandatory payments made by employees and employers to fund state benefits like the NHS and pensions. If you get these calculations wrong, Her Majesty’s Revenue and Customs (HMRC) will not send a friendly reminder. They will send a penalty notice.

As we move through 2026, the landscape of UK taxation has shifted significantly following the reforms introduced in the previous fiscal year. For business owners, HR managers, and accountants, understanding the current thresholds, rates, and filing obligations is not optional-it is critical for cash flow management and legal compliance. This guide breaks down exactly how much you need to pay, when you need to pay it, and how to avoid the most common pitfalls that trip up even experienced employers.

Understanding the Core Structure of NICs

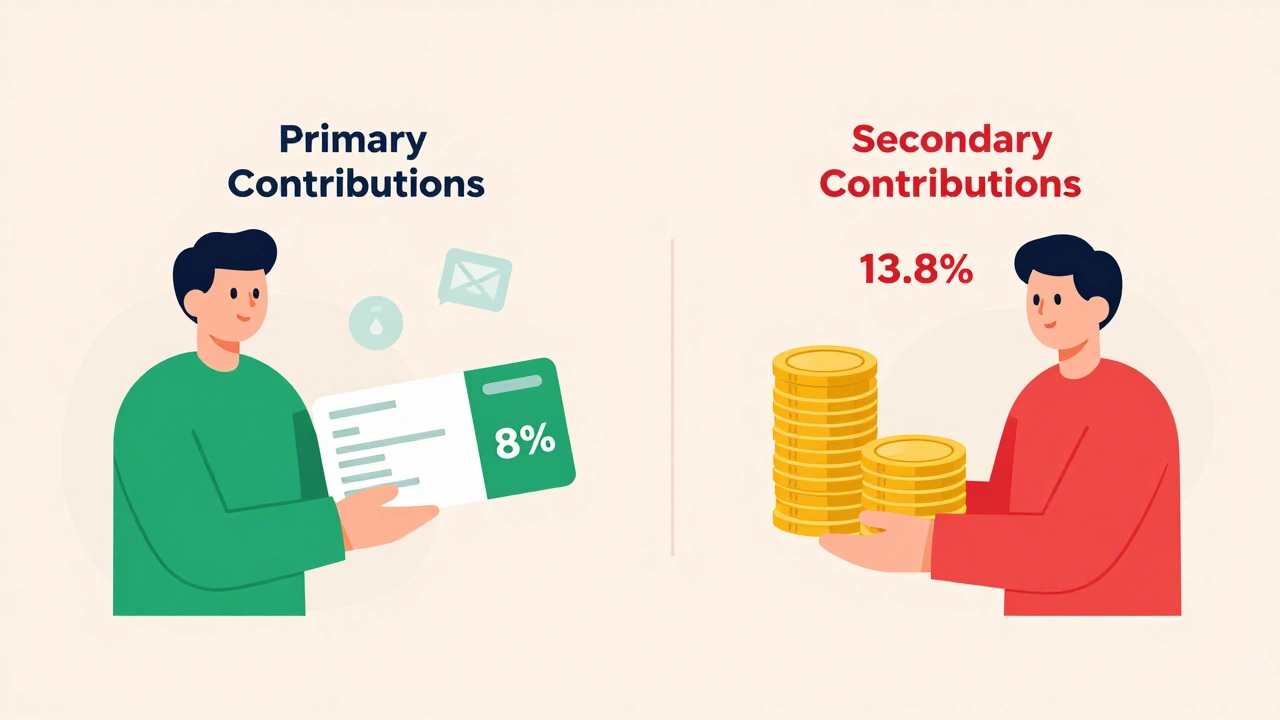

To calculate your obligations correctly, you first need to understand who pays what. National Insurance is split into two main categories for businesses: Class 1 contributions paid by employees and employers, and secondary contributions paid by the company itself. It is crucial to distinguish between these because they have different thresholds and rates.

Class 1 Primary Contributions are deducted directly from an employee's gross salary before they receive their net pay. These funds go toward the employee’s future State Pension and certain unemployment benefits. As an employer, you act as the collector, withholding this amount and passing it to HMRC along with Income Tax via the Pay As You Earn (PAYE) system.

Class 1 Secondary Contributions are paid entirely by the employer on top of the employee's salary. This is a direct business expense. Unlike primary contributions, there is no upper earnings limit for secondary contributions in most cases, meaning you pay this percentage on every penny of salary above the secondary threshold. Additionally, directors and self-employed individuals may fall under Class 2 or Class 4, but for standard employment contracts, Class 1 is the focus.

2026 Rates and Thresholds: What You Need to Know

The government adjusts National Insurance thresholds annually, usually in April. By May 2026, the new rates set at the start of the 2025-2026 tax year are fully in effect. Getting these numbers right is essential for accurate payroll processing. Below is a breakdown of the key figures you must use in your calculations.

| Category | Weekly Threshold | Monthly Threshold | Annual Threshold | Rate |

|---|---|---|---|---|

| Employee Lower Earnings Limit (LEL) | £123 | £533 | £6,515 | 0% (but builds entitlement) |

| Employee Primary Threshold (PT) | £242 | £1,048 | £12,570 | 8% (above PT up to UEL) |

| Employee Upper Earnings Limit (UEL) | £967 | £4,189 | £50,270 | 2% (above UEL) |

| Employer Secondary Threshold (ST) | £175 | £758 | £9,100 | 13.8% (above ST) |

Note that the Employee Primary Threshold aligns with the Personal Allowance for Income Tax, meaning most employees do not pay Income Tax or National Insurance on their first £12,570 of annual income. However, the Employer Secondary Threshold is lower. This creates a "gap" where an employee pays no NICs, but the employer still owes 13.8% on earnings above £9,100. This discrepancy is a common source of confusion for small business owners calculating total labor costs.

Step-by-Step Calculation Guide

Calculating NICs manually can be tedious, but understanding the logic helps you verify your payroll software. Let’s look at a practical example. Imagine you hire a marketing manager named Sarah. She earns £4,000 per month. How much does she pay, and how much do you pay?

- Determine the taxable base: Start with Sarah’s gross monthly salary of £4,000.

- Calculate Employee (Primary) NICs:

- Subtract the Primary Threshold (£1,048) from her salary: £4,000 - £1,048 = £2,952.

- This remaining amount is split between the main rate and the reduced rate.

- The difference between the Upper Earnings Limit (£4,189) and the Primary Threshold (£1,048) is £3,141. Since £2,952 is less than £3,141, all of it falls under the 8% rate.

- Calculation: £2,952 x 8% = £236.16.

- Sarah pays £236.16 in National Insurance.

- Calculate Employer (Secondary) NICs:

- Subtract the Secondary Threshold (£758) from her salary: £4,000 - £758 = £3,242.

- Apply the employer rate of 13.8% to the remainder.

- Calculation: £3,242 x 13.8% = £447.40.

- You pay £447.40 in National Insurance.

In this scenario, the total National Insurance cost associated with Sarah’s £4,000 salary is £683.56. This represents a significant portion of her compensation package. When budgeting for new hires, always factor in this ~17-20% overhead on top of gross salary to avoid cash flow surprises.

Filing Obligations and Real Time Information (RTI)

Gone are the days of sending paper forms once a year. The UK operates under a system called Real Time Information (RTI), which requires employers to report PAYE and NIC data to HMRC electronically each time they pay staff. This system ensures that tax and contribution data is up-to-date and reduces fraud.

Your obligations under RTI are strict:

- Full Payment Submission (FPS): You must send an FPS to HMRC on or before the day you pay your employees. This submission includes details of each employee’s pay, tax deducted, and NICs paid. It also acts as the employee’s payslip if you don’t provide one separately.

- Employer Payment Summary (EPS): Previously known as the End of Year Statement, the EPS is used to report things like maternity pay, paternity pay, or carer’s leave. If you don’t need to report any of these, you might not need to file an EPS, but check specific requirements for your business type.

- Payment Deadlines: You must pay the collected taxes and NICs to HMRC by the 22nd of the following month if you pay electronically (or the 19th if paying by cheque). For example, payroll processed in April must be paid by May 22nd.

Missing a deadline triggers immediate penalties. HMRC uses automated systems to detect late filings. A single late payment can result in a fixed penalty, while repeated failures lead to escalating fines based on the amount owed. In severe cases, persistent non-compliance can lead to director disqualification.

Common Pitfalls and How to Avoid Them

Even seasoned accountants make mistakes with National Insurance. Here are the most frequent errors and how to sidestep them.

Misclassifying Workers: One of the biggest risks in the UK gig economy is misclassifying an employee as a self-employed contractor. If HMRC determines that a worker is effectively an employee (due to control, mutuality of obligation, and substitution rules), they will reclassify them retroactively. This means you owe backdated NICs, plus interest and penalties. Always assess the working relationship using HMRC’s Check Employment Status for Tax (CEST) tool before signing contracts.

Ignoring Benefits in Kind (BiK): Did you give your director a company car? Provide private healthcare? Offer gym memberships? These are taxable benefits. You must pay Class 1A National Insurance on the cash equivalent value of these benefits. This is due by July 19th after the end of the tax year, separate from regular monthly payments. Failing to report BiKs is a classic audit trigger.

\nUsing Outdated Software: Payroll software updates automatically with legislative changes. If you are using outdated software or manual spreadsheets from 2024, you are likely applying old thresholds. Ensure your accounting provider confirms their software is updated for the 2025-2026 tax year rates.

Strategic Planning for Business Owners

While you cannot avoid paying National Insurance, you can manage its impact. For startups and small businesses, consider the following strategies:

- Salary vs. Dividends: Company directors often take a low salary (up to the Primary Threshold of £12,570) to avoid paying Income Tax and Primary NICs, then draw the rest of their income as dividends. Dividends do not attract National Insurance. However, you still pay Corporation Tax on profits before distribution. Consult a tax advisor to optimize this mix.

- Pension Contributions: Employers must auto-enroll eligible staff into a workplace pension. Minimum employer contributions are typically 3% of qualifying earnings. While this is an additional cost, it is tax-deductible for the business and helps meet legal obligations without triggering higher NIC bands if structured correctly within salary sacrifice schemes (though rules here are tight).

- Apprenticeship Levy: If your annual payroll exceeds £3 million, you also pay the Apprenticeship Levy at 0.5%. This is calculated separately from NICs but relates to the same payroll data. Keep an eye on this threshold if you are growing rapidly.

Proactive management of these costs ensures that your business remains compliant while maximizing available tax efficiencies. Regular reviews with a qualified accountant can uncover savings that offset the rising cost of labor.

What happens if I pay National Insurance late?

HMRC charges interest on overdue amounts from the due date until payment. Additionally, you face fixed penalties for late filing and late payment. The first penalty is usually small, but subsequent penalties increase significantly. Repeated offenses can lead to public listing of your debt and potential prosecution for serious evasion.

Do I need to pay NICs for part-time employees?

Yes. National Insurance is based on earnings, not hours worked. If a part-time employee earns above the Primary Threshold (£242 weekly or £1,048 monthly), they pay primary NICs. If they earn above the Secondary Threshold (£175 weekly or £758 monthly), you pay secondary NICs. The calculation method remains the same as for full-time staff.

How do I handle NICs for contractors versus employees?

Genuine self-employed contractors do not pay Class 1 NICs through PAYE. They handle their own Class 2 and Class 4 contributions via Self Assessment. However, if the worker meets the criteria for employment (IR35 rules apply inside IR35), you must treat them as an employee for tax purposes, deducting PAYE and NICs. Misclassification carries high financial risks.

When is the deadline for paying NICs in 2026?

For most businesses paying electronically, the deadline is the 22nd of the month following the payroll period. For example, January payroll is due by February 22nd. If the 22nd falls on a weekend or bank holiday, the deadline moves to the next working day. Monthly payers must adhere strictly to this schedule.

Can I reclaim overpaid National Insurance?

Yes, if you have overpaid NICs due to an error, you can claim a refund from HMRC. You must submit a correction via your payroll software or contact HMRC directly. Refunds are typically processed within 30 days, provided the claim is valid and supported by correct records. Keep detailed payroll logs to substantiate any claims.